Last year after making the decision to move to Galway Ireland we set out to find office space and a bank to enable our operations to function. As consultants and accountants, we have been exposed to or used some of the latest technology and best practices from a variety of industries across the Globe. The Canadian Banking system is dominated by a few large players, just like in Ireland. However, we were surprised to find that their was a huge technology gap between the two markets. We looked at 3 players (Bank of Ireland, AIB and Ulster Bank) and found that they were all using basic platforms that resembled functionality and technology from the 90’s. Why was tech proud Ireland so behind?

Here are some of the features we are used to working with and think should be employed by Irish Banks. Have a peak and tell us which one would be most useful to you or your business with a poll at the end.

1.Mobile Check deposit-Deposit a check via your mobile phone

2. Receive and send money using only your email, and no Banking details.

3. Add a Bill or Payee by simply scanning it into your banking app? This uses the same technology as check deposit above.

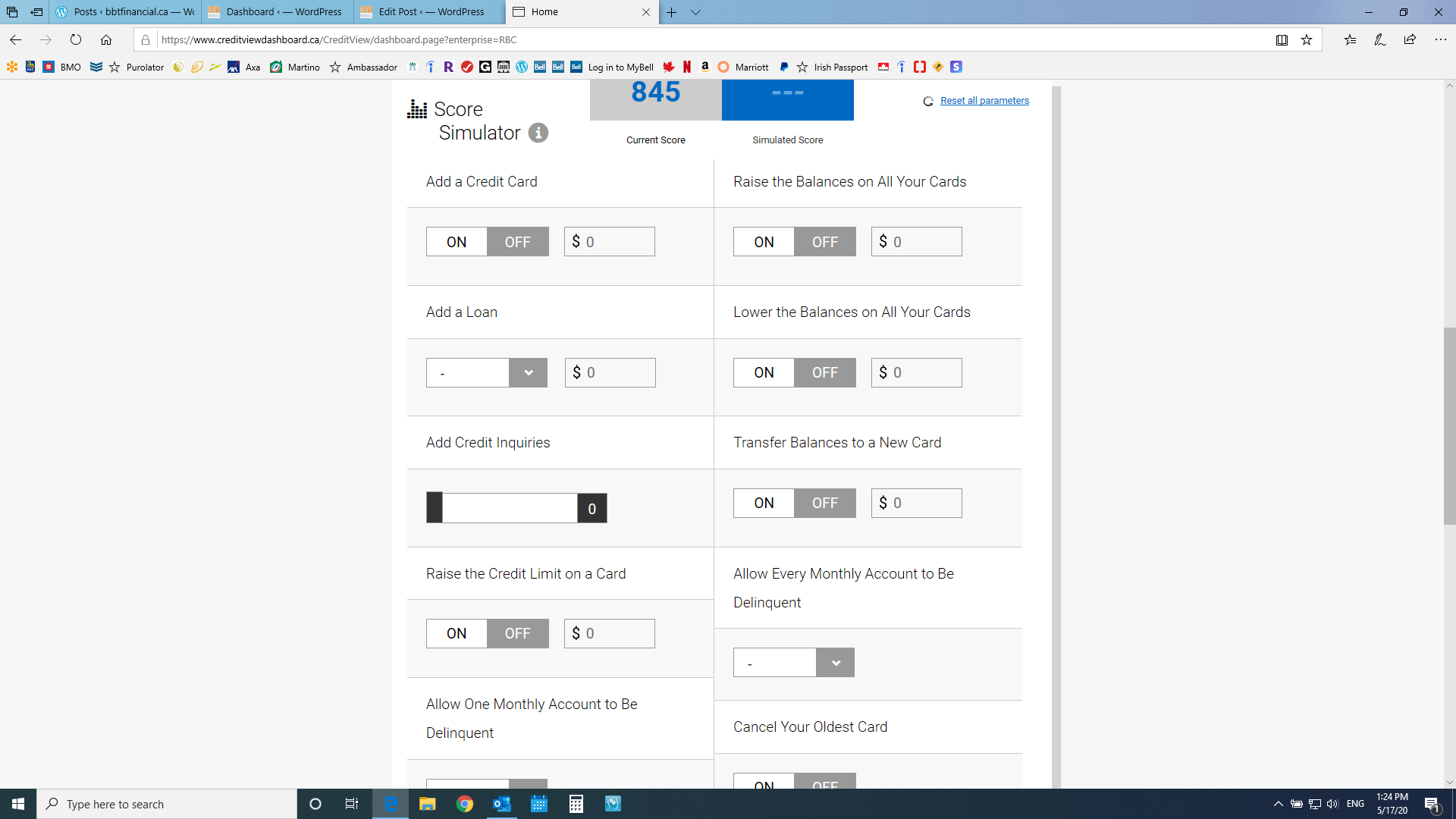

4. Current Credit Score and Credit Score simulator which reflects how your situation may change based on your plans.

So there you have it. Our top 4 tech choices we wish Irish banks employed. There are loads more features we’d like to see but these were the most useful to regular customers. Let us know which one you value the most? Hopefully someone somewhere important will see this and start the ball rolling.

Thank you for Reading